For individuals and families struggling to rein in spending and gain control of their finances, the Envelope System offers a time-tested, tangible solution. This cash-based budgeting method involves allocating physical cash into labeled envelopes for various spending categories—like groceries, gas, and entertainment—for a set period, typically a pay cycle. Once the cash in an envelope is gone, spending in that category must stop until the next cycle, effectively creating a hard limit. The system works because it forces a psychological and behavioral shift, making spending a conscious, visible act rather than an invisible swipe of a card, which is why it remains one of the most powerful tools for eliminating debt and building financial discipline.

How the Envelope System Works: A Step-by-Step Guide

At its core, the envelope system is brilliantly simple. It replaces the abstract nature of digital transactions with the concrete reality of physical cash. By following a few straightforward steps, anyone can implement this method to transform their financial habits.

Step 1: Track Your Spending and Create a Budget

Before you can tell your money where to go, you must first understand where it is currently going. The crucial first step is to track every single expense for at least one month. Use a notebook, a spreadsheet, or a budgeting app to log every coffee, subscription, and grocery run.

Once you have a clear picture of your spending habits, you can create a realistic budget. A zero-based budget is often the most effective partner to the envelope system. This approach requires that your total income minus all your expenses (including savings and debt payments) equals zero, ensuring every dollar has a specific job.

Step 2: Identify Your Variable Spending Categories

Your budget consists of two types of expenses: fixed and variable. Fixed expenses are consistent costs like your mortgage or rent, car payments, and insurance premiums. These are typically paid automatically or by check and do not fit into the cash envelope model.

The envelope system is designed for your variable expenses—the costs that fluctuate each month. These are the areas where overspending commonly occurs. Common categories include groceries, restaurants, gas, personal care, entertainment, clothing, and household supplies.

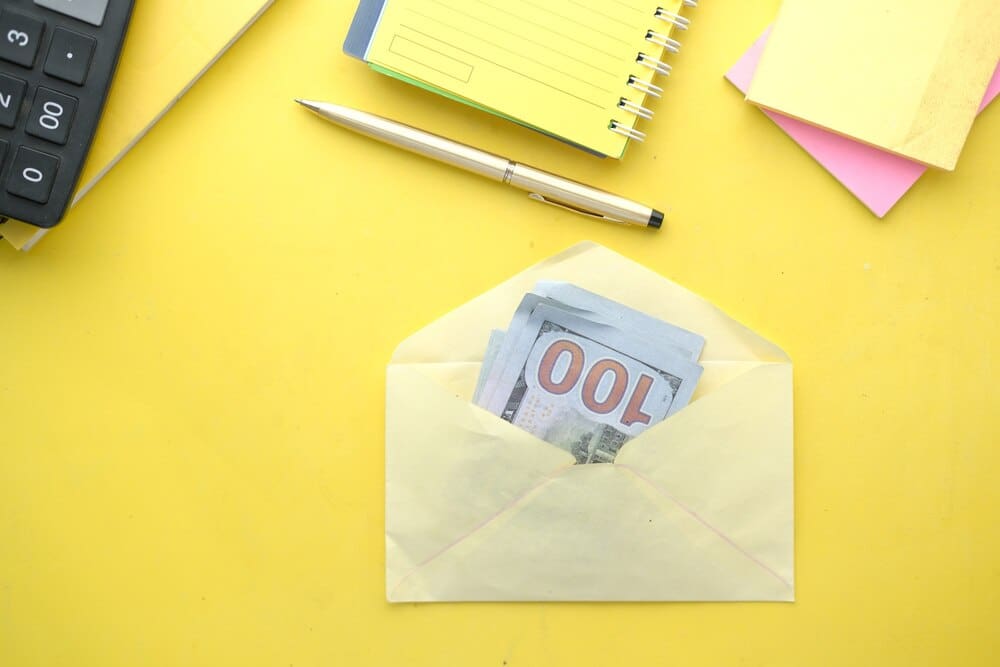

Step 3: Get Your Envelopes and Your Cash

This step is where the system becomes tangible. After each payday, go to your bank and withdraw the total amount of cash you have budgeted for all your variable spending categories. You will need a physical envelope for each of these categories.

You can use plain white envelopes from an office supply store or purchase specialized budgeting envelopes, which often come with printed trackers on the outside. Clearly label each envelope with its category (e.g., “Groceries”) and the budgeted amount for the pay period (e.g., “$400”).

Step 4: Stuff the Envelopes

With your cash and labeled envelopes in hand, you can now perform the ritual of “stuffing.” Place the exact budgeted amount of cash into its corresponding envelope. For example, if your budget allocates $150 for gas and $80 for entertainment, you will put $150 in the “Gas” envelope and $80 in the “Fun Money” envelope.

This physical act reinforces your financial plan. You are visually and physically dedicating specific funds to their intended purpose, creating a strong mental commitment to stick to your budget.

Step 5: Spend Only from the Envelopes

This is the most critical part of the process: discipline. When you go to the grocery store, you take only the “Groceries” envelope with you. When you pay, you use the cash from that envelope. Any change goes directly back into the same envelope.

The golden rule is absolute: once an envelope is empty, you cannot spend any more money in that category until the next pay period. Resist the temptation to “borrow” from other envelopes, as this defeats the purpose of the system. If you run out of grocery money, you make do with what’s in your pantry until your next payday.

The Psychology Behind Why Cash Budgeting is So Effective

The enduring success of the envelope system is rooted in behavioral psychology. It leverages human nature to encourage better financial decisions, something that swiping a credit card is designed to bypass.

The Pain of Paying

Neuroscientists and behavioral economists talk about the “pain of paying.” This refers to the negative emotion we feel when we part with our money. Studies have shown that this pain is significantly higher when using physical cash compared to credit cards or digital payments.

Watching a cashier take your last $20 bill from an envelope creates a tangible sense of loss. This friction makes you think twice about impulse purchases and encourages you to seek better value for your money. Credit cards, on the other hand, decouple the purchase from the payment, making spending feel abstract and painless in the moment.

Forced Mindfulness and Intentionality

The envelope system forces you to be mindful of your spending. Before making a purchase, you must check your envelope to see if you have enough cash. This simple act breaks the pattern of mindless consumption.

You can physically see your resources dwindling as the cash level in the envelope drops. This visual cue is a powerful motivator to spend intentionally and prioritize what is truly important, rather than succumbing to wants that don’t align with your financial goals.

Breaking the Debt Cycle

Perhaps the most significant benefit of the envelope system is that it makes it impossible to spend more money than you have. You cannot overdraft a cash envelope. This simple constraint is a powerful antidote to the cycle of credit card debt.

By living strictly on the cash you have on hand for your variable expenses, you eliminate the possibility of accumulating high-interest consumer debt. This provides an immense sense of control and peace of mind, empowering you to use your remaining income to aggressively pay down existing debt or build savings.

Who Should Use the Envelope System? (And Who Might Not)

While incredibly effective, the envelope system isn’t a one-size-fits-all solution. Its suitability depends on an individual’s personality, lifestyle, and financial situation.

Ideal Candidates for the System

This method is particularly powerful for visual and tactile learners who benefit from a hands-on approach. It is an excellent tool for those who consistently overspend on credit cards and struggle with impulse buys. Couples can also find it highly effective for managing shared household expenses, as it provides a transparent and mutually accountable system.

Potential Drawbacks and Considerations

The primary drawback is the inconvenience and security risk of carrying cash. In an increasingly digital world, some transactions, especially online purchases, are difficult or impossible to make with cash. Furthermore, if you lose an envelope or are a victim of theft, the cash is gone for good.

Another consideration is that the system does not help build a credit history, which is essential for future loans like a mortgage. Finally, tracking expenses for tax purposes or annual reviews can be more cumbersome, as it requires diligent manual record-keeping of cash transactions.

Adapting the Envelope System for the Digital Age

For those who find the idea of carrying cash impractical but are drawn to the system’s principles, modern technology offers several excellent alternatives that mimic the envelope methodology.

The Rise of Digital Envelope Apps

A host of budgeting apps have been developed specifically to replicate the envelope system digitally. Apps like Goodbudget and YNAB (You Need A Budget) allow you to create virtual “envelopes” or categories. You fund these envelopes from your linked bank account and, as you spend using your debit or credit card, you assign each transaction to its corresponding envelope, watching the available balance decrease in real-time.

The Hybrid Approach: Cash and Digital

A hybrid approach offers a flexible middle ground. You can use physical cash envelopes only for the one or two categories where you overspend the most, such as “Dining Out” or “Hobbies.” For other necessities like groceries or gas, you can continue using a debit card for convenience while tracking the spending within a budgeting app.

Using Multiple Bank Accounts

Another strategy is to use multiple free checking accounts as your “envelopes.” You can open several accounts and name them after their purpose (e.g., “Bills & Fixed,” “Groceries & Gas,” “Personal Spending”). After each payday, you automatically transfer the budgeted amounts into each account. You then use the specific debit card tied to that account for its designated purpose only, creating the same single-purpose discipline as a physical envelope.

Ultimately, the Envelope System—whether practiced with physical cash, digital apps, or a hybrid model—is more than just a budgeting tactic. It is a powerful behavioral tool that fundamentally reshapes your relationship with money. By forcing intentionality and creating a healthy friction in the spending process, it empowers users to move from a state of financial anxiety to one of control, clarity, and confidence.